Have you ever wondered if all debt is bad for you? It’s a common question because debt often feels like a burden.

But what if some debt could actually help you grow your wealth or reach your goals faster? Understanding the difference between good debt and bad debt can change the way you handle your money—and your future. You’ll discover how to spot which debts work in your favor and which ones drag you down.

Keep reading to learn how to take control of your finances and make smarter choices that benefit you in the long run.

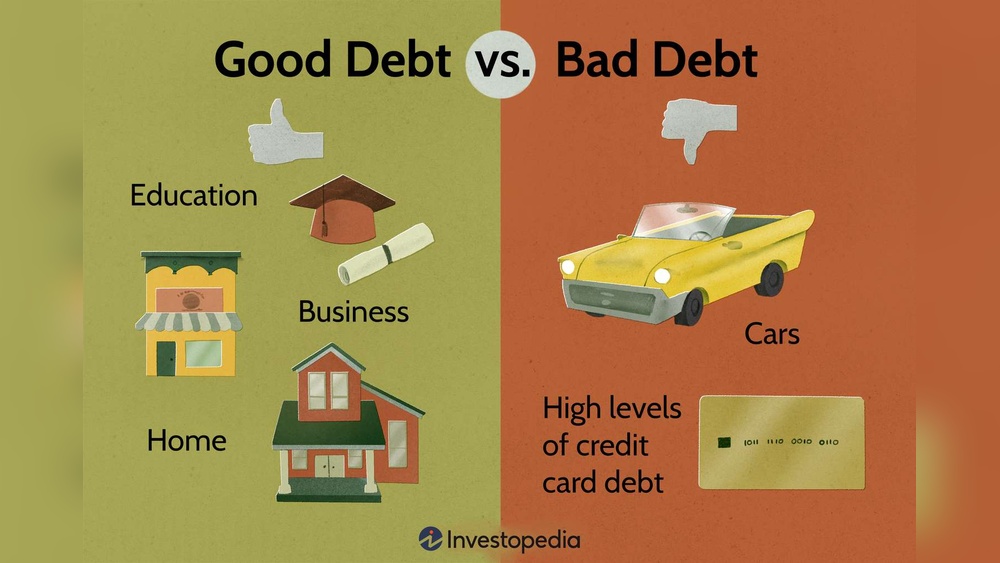

Good Debt Vs Bad Debt

Understanding the difference between good debt and bad debt helps you manage money better. Good debt can build your future, while bad debt can cause stress. Knowing the difference keeps your finances healthy and your goals on track.

Characteristics Of Good Debt

Good debt helps you gain something valuable. It often funds education, a home, or a business. This debt usually has low interest rates. It can increase your future income or net worth. Paying off good debt can improve your credit score.

Traits Of Bad Debt

Bad debt pays for things that lose value fast. Credit card debt and payday loans are common examples. This debt usually has high interest rates. It can trap you in a cycle of borrowing. Bad debt hurts your credit and financial health.

How Debt Impacts Financial Health

Debt affects your ability to save and invest. Good debt can help you grow wealth over time. Bad debt drains your money with high interest payments. Managing debt wisely keeps your financial stress low. Tracking debt helps you make smarter money choices.

Credit: www.westernsouthern.com

Types Of Good Debt

Good debt helps build wealth or improve your future. It often has lower interest rates and a clear return on investment. Knowing the types of good debt can help you make smart financial choices.

Student Loans

Student loans pay for education that can increase your earning power. A good education often leads to better job opportunities. This type of debt is an investment in your future skills.

Mortgage Loans

Mortgage loans let you buy a home, which usually grows in value. Owning a home builds equity over time. This debt can be good if you plan to live in the home long term.

Business Loans

Business loans help start or grow a company. They can lead to higher income and new opportunities. Smart use of business debt can increase your financial stability.

Investments In Appreciating Assets

Loans for assets like real estate or equipment can increase in value. These investments can create income or grow your wealth. Such debt is good if the asset gains more than the loan costs.

Common Bad Debts

Bad debts can hurt your financial health. They often come with high interest rates and little benefit. Knowing common bad debts helps you avoid money traps. These debts usually drain your resources instead of building your future.

Credit Card Debt

Credit card debt grows fast due to high interest rates. Missing payments adds fees and lowers your credit score. Using credit cards for daily expenses can trap you in debt. Paying only the minimum balance keeps you paying for years.

Payday Loans

Payday loans offer quick cash but cost a lot. Their interest rates are extremely high. Many borrowers struggle to repay on time. This debt can lead to a cycle of borrowing and debt.

Auto Loans For Depreciating Vehicles

Auto loans on cars that lose value quickly are risky. You may owe more than the car is worth. This situation is called being “underwater” on your loan. It can cause financial loss if you sell or trade in the car.

Unnecessary Consumer Debt

Buying items you do not need on credit creates bad debt. This includes gadgets, clothes, or luxury goods. These purchases lose value fast and add monthly payments. Such debt does not build wealth or improve your life.

Evaluating Debt For Smart Decisions

Evaluating debt carefully helps make smart financial decisions. Not all debt is bad. Some debts can help build wealth or improve your life. Others might cause financial stress and limit your future choices. Knowing the difference is important. Consider these key points before taking on debt.

Interest Rates And Terms

Interest rates affect how much debt costs over time. Lower rates mean less money paid in interest. Shorter loan terms usually save money on interest. Long terms may lower monthly payments but increase total interest. Check for fees and penalties too. Understand the full cost before borrowing.

Purpose And Outcome Of Debt

Good debt often funds education, a home, or business growth. These can increase your income or value over time. Bad debt usually pays for things that lose value fast. Like expensive gadgets or vacations. Think about the result of your debt. Will it help your future or hold you back?

Debt-to-income Ratio

Your debt-to-income ratio shows how much you owe versus earn. A high ratio means more income goes to debt payments. This can make borrowing harder and riskier. Aim to keep this ratio low. It helps maintain financial balance and peace of mind.

Long-term Financial Goals

Debt decisions should fit your long-term plans. Avoid debt that conflicts with your goals. For example, don’t take on heavy debt if you want to save for retirement soon. Plan debt around your future needs. Align borrowing with your life path and dreams.

Managing And Reducing Bad Debt

Managing and reducing bad debt is key to improving your financial health. It takes effort and clear steps. Starting with a plan helps you stay on track. Small changes make a big difference over time.

Debt Consolidation Options

Debt consolidation means combining several debts into one. It can lower your interest rate and monthly payments. This makes debt easier to handle. Look for loans or credit cards with better terms. Choose options that fit your budget and goals.

Budgeting Strategies

Create a budget that tracks your income and spending. Prioritize paying off bad debt quickly. Cut non-essential expenses to free up money. Set aside funds each month for debt repayment. Staying consistent helps reduce debt faster.

Negotiating With Creditors

Contact creditors to discuss your debt situation. They may offer lower interest rates or payment plans. Explain your financial difficulties honestly. Many creditors prefer working with you rather than risking default. Negotiation can reduce your total debt burden.

Seeking Professional Help

Debt counselors can guide you through tough financial times. They offer advice and help create a repayment plan. Professionals can negotiate with creditors on your behalf. Look for reputable agencies with good reviews. Getting help can speed up your debt recovery.

Credit: www.northamericancompany.com

Leveraging Good Debt For Wealth Building

Leveraging good debt can help build wealth over time. It means using borrowed money wisely to create value. Good debt often funds assets that grow or generate income. This approach can increase your net worth and financial stability.

Using good debt requires careful planning and discipline. Understanding how to manage it can lead to long-term benefits. The key is to borrow for investments that have a positive return.

Using Debt To Invest

People often use loans to invest in real estate or education. Real estate can increase in value and generate rental income. Education can improve job opportunities and earning potential. Borrowing for these purposes can be a smart financial move.

Investing with debt means the returns must be higher than the loan cost. This strategy takes effort and good judgment to succeed.

Tax Advantages Of Certain Debts

Some debts come with tax benefits. Mortgage interest is often tax-deductible. This lowers the overall cost of borrowing. Student loan interest may also be deductible in some cases. These advantages make certain debts more affordable and attractive.

Always check current tax laws to understand possible benefits.

Building Credit Score

Good debt helps build a strong credit score. Timely payments show lenders you are reliable. A good credit score leads to better loan offers. This reduces borrowing costs over time. Using debt responsibly is key to improving credit history.

It takes patience and consistent payments to build credit.

Timing Debt Repayment

Paying off debt at the right time matters. Early repayment can save interest costs. But sometimes, keeping debt longer can free cash flow for other uses. Balancing repayment schedules helps manage finances better. Planning payments avoids late fees and credit damage.

Timing your debt repayment supports financial growth and stability.

Credit: www.northamericancompany.com

Frequently Asked Questions

What Is Good Debt Versus Bad Debt?

Good debt is an investment that grows your wealth or skills. Bad debt is borrowing for items that lose value quickly or don’t generate income. Understanding this helps manage finances better and avoid costly mistakes.

How Can I Identify Good Debt?

Good debt typically funds education, real estate, or business growth. It usually has low interest and long-term benefits. If the debt improves your financial future, it’s likely good debt.

Why Is Bad Debt Harmful?

Bad debt often comes with high interest and no financial return. It can reduce your credit score and limit future borrowing options. Avoiding bad debt helps maintain financial stability.

Can All Debts Be Classified As Good Or Bad?

Most debts fit into good or bad categories, but some fall in between. It depends on the purpose, interest rate, and repayment terms. Evaluate each debt based on its impact on your finances.

Conclusion

Good debt helps build your future and grow your wealth. Bad debt drains your money and adds stress. Choose debt that improves your life, not harms it. Always think carefully before borrowing money. Managing debt wisely leads to better financial health.

Remember, not all debt is equal. Use this knowledge to make smart choices. Your financial peace depends on how you handle debt.